- Simply avoid products that are complicated to understand, unless you have a lot of time on your hands

22. Unregulated Investment Product

- MLM, wine investment etc, you name it, avoid it!

23.Investing In A Life Annuity

- The book recommends putting your money in a life annuity, but I think you are better off parking your money with SSB(Singapore Saving Bond), which is backed by the government and either in the STI ETF or Singapore ABF bond

24. Writing A Will

- Definitely a must for retirees!

25.Experience Of Consumer

- various scenario of people with a different financial and family background,nothing much here

26.Commonly used words and what they mean

Annual management fee

- This is the fund management fee, charged by the fund manager to manage your fund

- Shows the benefit you get from the insurance before you sign the dotted line

- Do read carefully, if in doubt refer back to the company

Bid price

- The selling price of your stock

Bond

- A bond is like a loan

- When you "buy" a bond, you effectively "lend" the government or company some money, in return for some interest over the next few years

- The ability of the government or the company to repay this interest is known as the creditworthiness of the government/company

- A common measurement is this creditworthiness is the credit rating of the government/company(e.g the bond is rated AAA)

- A bond issue by the government is a government bond,a bond issue by the company is a corporate bond

Offer price

- Price at which you buy the shares, also known as "asking price" or "selling price" or "buying price"

Sales charge

- the charge you pay initially when you buy a financial product

Shares/stocks

- This is a paper which represents a unit of ownership in a listed company.

- With a purchase of a stock/share, you own a small fraction of the company, depending on how many shares you have accumulated'

All in all,that's is a quick summary of the book:Practical Guide on Financial Planning,in the next few post,we are going to learn on how to read financial statement which is useful for long term investor(and also short term investor aka traders),do look forward to it!

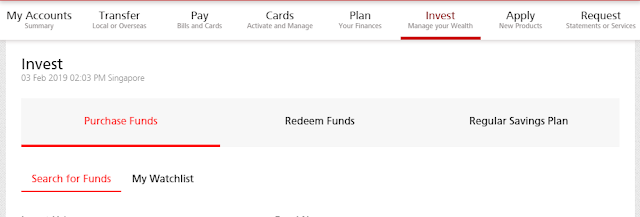

Step 7)Select regular saving plan(red circle)

Step 7)Select regular saving plan(red circle)